June 2019 | Signature Research

Digital at the Speed of Private Equity: How to Increase EBITDA Through Digital Investments in the Mid-Market

In the sky-high valuation environment that has defined the private equity market in recent years, the need to drive higher EBITDA returns is an imperative.

Get the full reportIn our survey of 100 mid-market PE firms, we found that digital is becoming a crucial part of the PE playbook—but not all firms are preparing to invest in digital effectively. Here are some of the key findings from our survey.

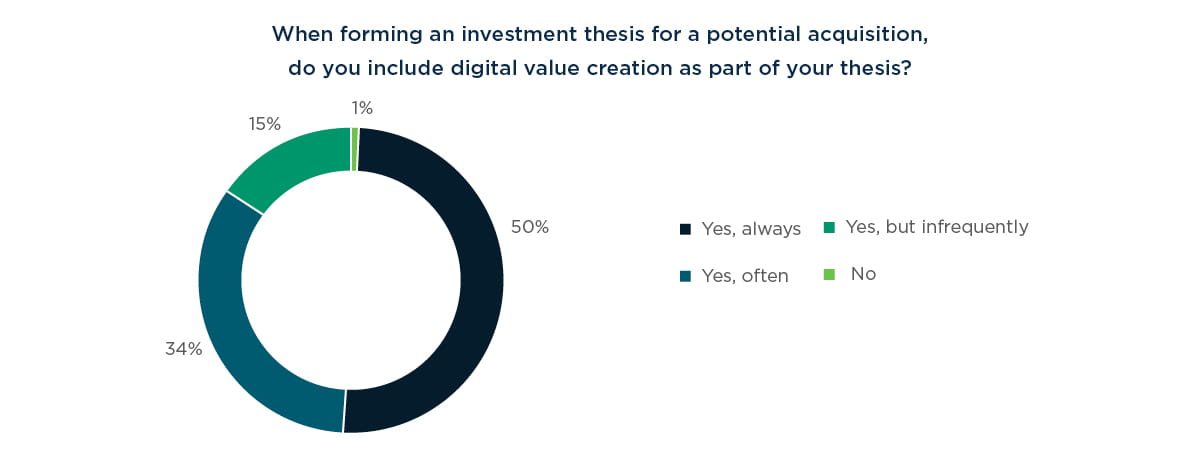

- PE firms appreciate the value of digital: Half of our respondents say they always include digital value creation as part of their investment thesis, and another 34% say they often include it.

- Not all GPs lay the groundwork necessary for digital success: Only 42% of General Partner (GP) respondents say their firm has a standard definition of digital that everyone aligns to. In addition, 40% of respondents say that half or fewer of the companies they own have a documented digital strategy.

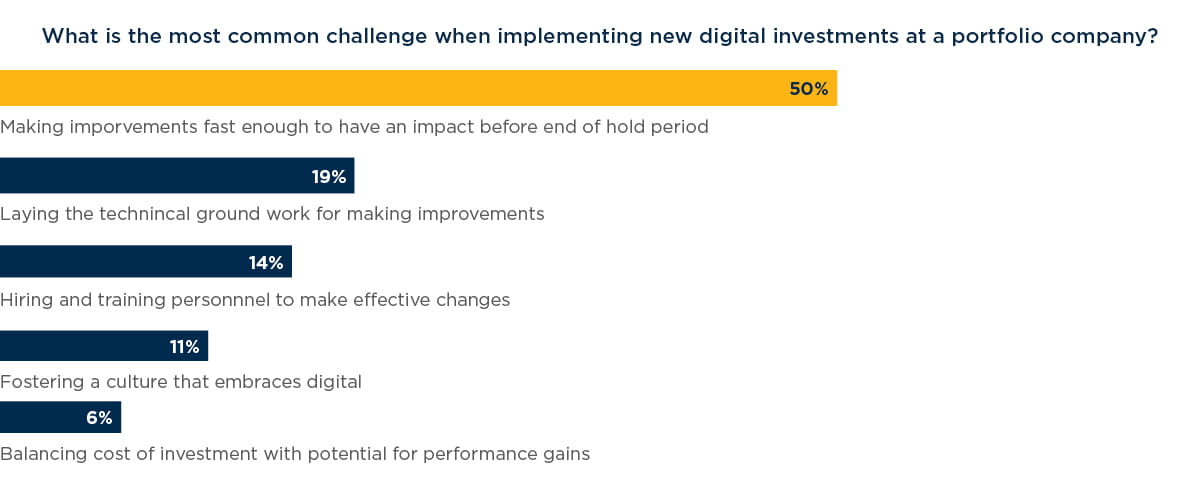

- Driving change and value over the hold period represents a top challenge: Fifty percent of PE executives say that making improvements quickly enough to have an impact before the end of the hold period is the greatest barrier to digital investment. As a result, 84% of respondents say they aim to implement a digital program at a portfolio investment within the first year after acquisition, and 26% try to do so within six months.

- Digital investment improves a portfolio company’s exit price: More than eight in ten (82%) respondents say they view mature digital investments at a portfolio company as a value driver at exit. Three-quarters (75%) say they also make digital investments in order to improve the exit price for a portfolio company without the expectation of performance gains before the sale.

Introduction

Digital transformation is fundamentally altering the way all industries do business. From healthcare to manufacturing to software and retail, customer expectations are changing, business models are being upended, and the pace at which technology is advancing is demanding unprecedented agility from management teams.

Indeed, the digital world poses specific challenges for private equity (PE), which invests in and operates companies that span different sectors, sizes, and stages of digital maturity—for relatively short periods of time. But it also poses significant opportunities: As experts in value creation, PE firms are poised to benefit from a focus on digital. When done well, it is a highly effective way to deliver efficiency improvements, revenue and earnings growth, and ensure a high pricing multiple at exit.

Yet, many PE firms are not fully equipped to seize the digital opportunities available to their portfolio companies, as our survey of 100 U.S. mid-market fund managers, conducted in partnership with Mergermarket, demonstrates.

In the sky-high valuation environment that has defined the PE market in recent years, the need to identify innovative and effective investment angles to create value has never been more pressing. The ability of firms to develop digitally led investment theses, carry out effective digital diligence, and deliver on their strategies will separate the industry’s best and weakest performers.

From our perspective, it will define PE’s next chapter.

Chapter 1: Define digital and formalize a strategy to create a foundation for success

Deciding there is value in digital

Value creation is PE’s forte, and in the current era, digital technologies can hold the greatest potential for creating value. But PE can be skeptical when it comes to digital projects, often viewing them as a cost center or taking too long to deliver ROI before sale. However, the evidence shows otherwise.

A previous study found that businesses can increase their revenue by an average of 23% through digital, with new product and service offerings contributing the highest revenue growth across all companies.1 In the middle market specifically, companies achieve an average 27.5% ROI on their digital projects, and that percentage rises to 39% for those that spend at least 10% of their revenue on digital, according to a separate study by the Middle Market Center.

A critical factor, of course, is timing. The latter study shows that on average, it takes three years for such investments to deliver results, and in some cases closer to five years. While the timeframe may be viewed as lengthy by some, a strategic digital plan can drive competitive advantages for firms and can substantially increase value at the point of exit.

In our survey of PE firms, value creation from digital is top-of- mind: Half of respondents say they always include digital value creation as part of their investment thesis. Another 34% say they often include it. But in reality, how are they planning and executing these strategies? Are they including digital more aspirationally, or are investments going as planned?

But first, define digital

The first challenge with digital, we found, is defining it. Only 42% of GP respondents to our survey say their firm has a standard definition of digital that everyone aligns to. While not surprising—as consultants, we deliver digital work across dozens of organizations that all define it differently—this poses a significant challenge to deriving value. If you’re not aligned on a definition, how can you decide where to create and measure value?

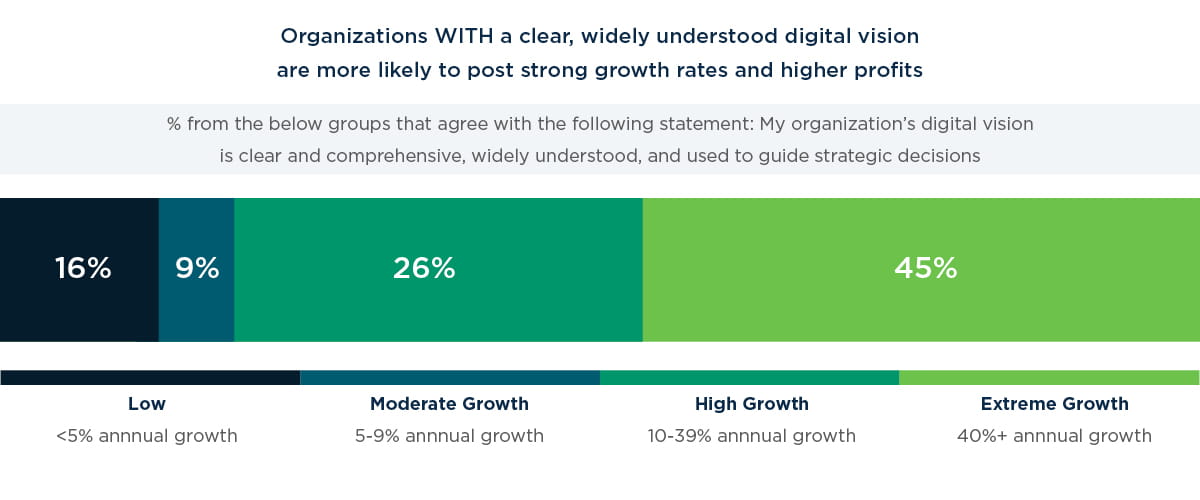

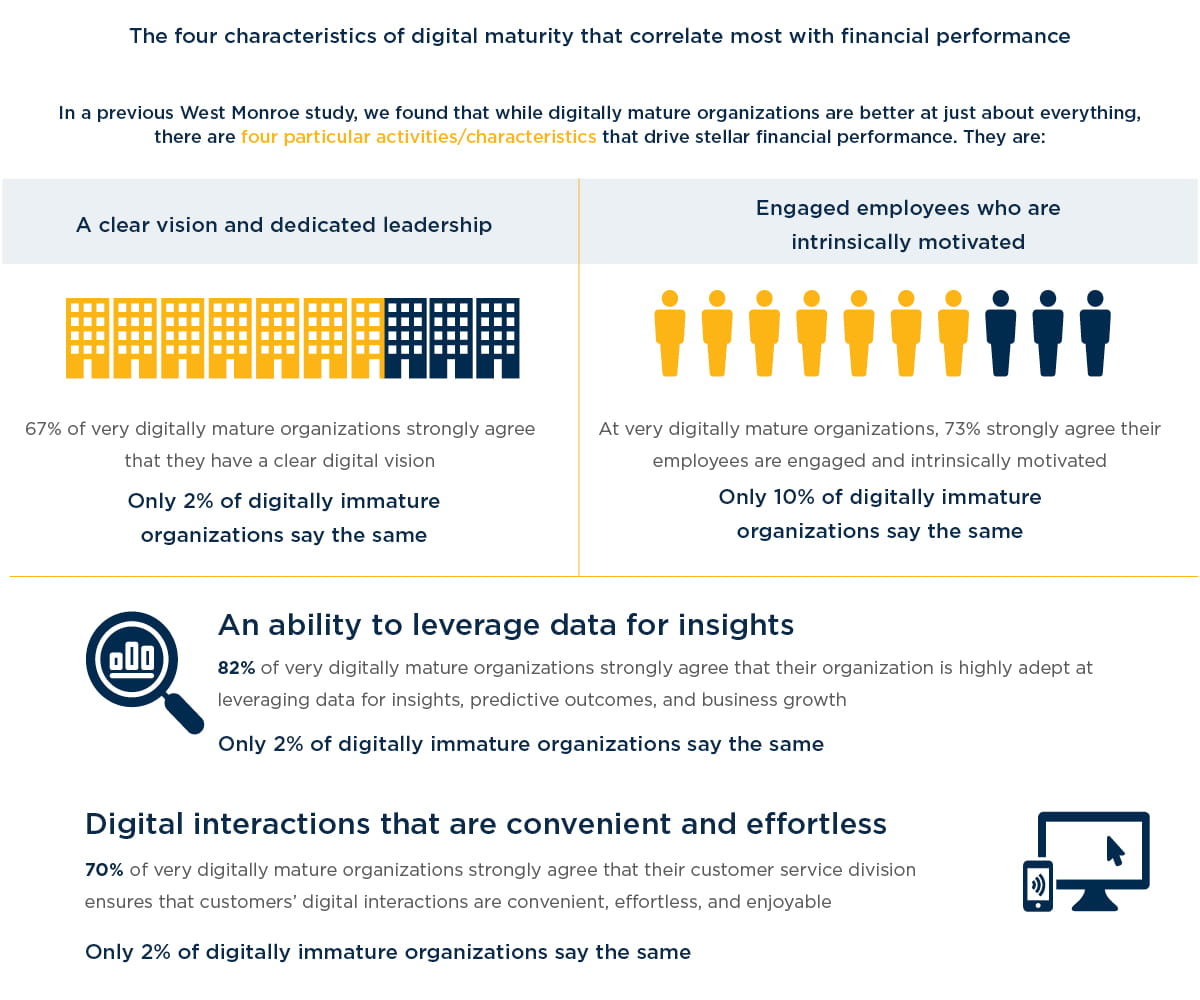

Seeking out a universal definition across industries, or even within the private equity industry, is challenging. But PE firms can create certainty by defining digital at least for their own portfolio—and they should. Organizations that have a clear, widely understood digital vision that guides strategic decisions are more likely to post strong growth rates and higher profits; this was a primary finding in West Monroe’s 2018 study, “Digital Leaders: Learn from Digitally Mature Companies to Grow Revenue and Profits.“

Defining digital is one step, but here’s where the process may break down: The GPs we surveyed indicate that they often do not formalize a digital investment strategy at their portfolio companies—a key step in maximizing the potential of a given business, says Nick Hahn, a director of digital at West Monroe. Specifically, 40% of our respondents say that half or fewer of the companies they own have a documented digital strategy.

“A documented digital strategy does one crucial and often overlooked thing: It identifies and prioritizes the highest potential digital value creation areas for the business,” Hahn says. “If you don’t go through the exercise of identifying and especially prioritizing well defined, strategically aligned value creation opportunities, and instead become enamored with a particular hot technology or pet idea, you can spend a lot of time, effort, and money and see poor results.”

Chapter 2: Focus on your digital efforts and be pragmatic to maximize returns

PE faces a challenge when it comes to digital, given the nature of their investment lifecycle. Hold periods are finite and often shorter than what is required to complete digital transformation, meaning sponsors need to think carefully about which projects to prioritize. Many companies come up with a list of dozens of initiatives and try to implement all at once, but this is almost never effective—it requires too much change too quickly, and spreads resources too thin.

“A reason that companies move slowly, and many are not seeing success, is that they try to do far too many things too soon,” says West Monroe’s Nick Hahn. “Even doing two or three things is very difficult given the typical level of change required and the potential lack of experience with digital strategy and implementation at a given portfolio company. Instead, it is best to think big but execute small.”

When considering the best approach to making digital investments at a new portfolio company, there is no one right place to start. It is wholly dependent on the business and what it is trying to achieve, as well as its level of digital maturity, the level of competition in the company’s sector, their advantages in the marketplace, and other factors.

This is especially true given the potential scope for digital investment, which can help to optimize everything from revenue growth—such as developing reporting frameworks that highlight growth areas and reveal underperforming areas of the business, or creating new adjacent services to bolster customer engagement—through to streamlining operations by automating previously manual processes.

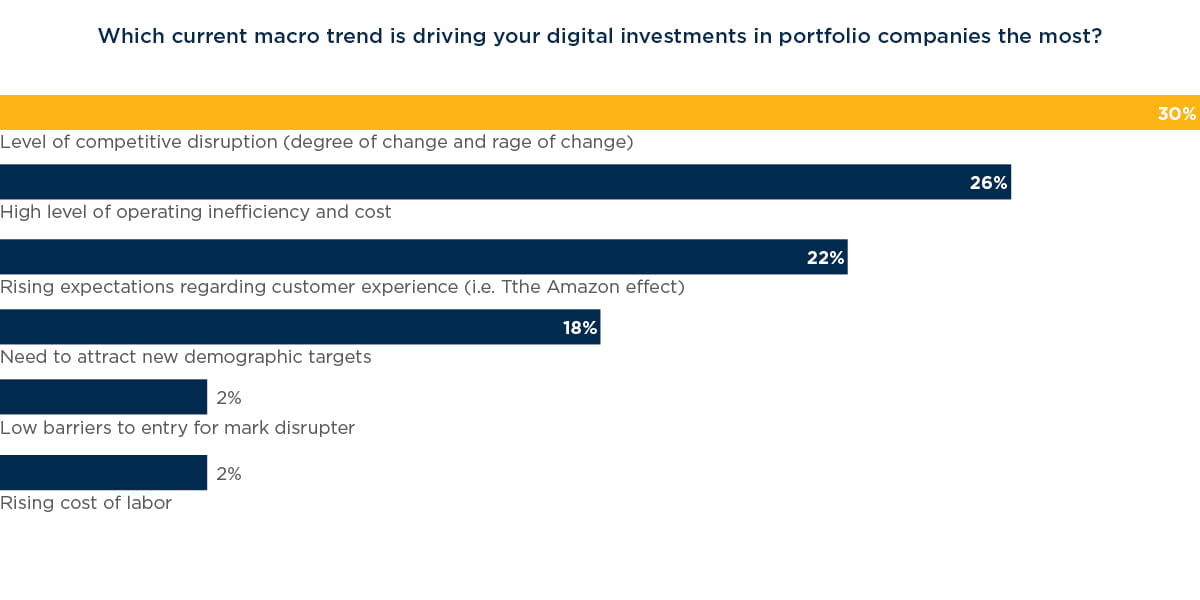

The need for digital, though, is widely felt and driven equally by both external market forces and internal constraints. Our survey respondents reported on the macro trends driving their digital investments: 30% pointed to

the level of competitive disruption, including the degree and rate of change, 26% report a high level of operating inefficiency and cost, and 22% cite the rising expectations regarding customer experience.

Narrowing down the list of digital opportunities

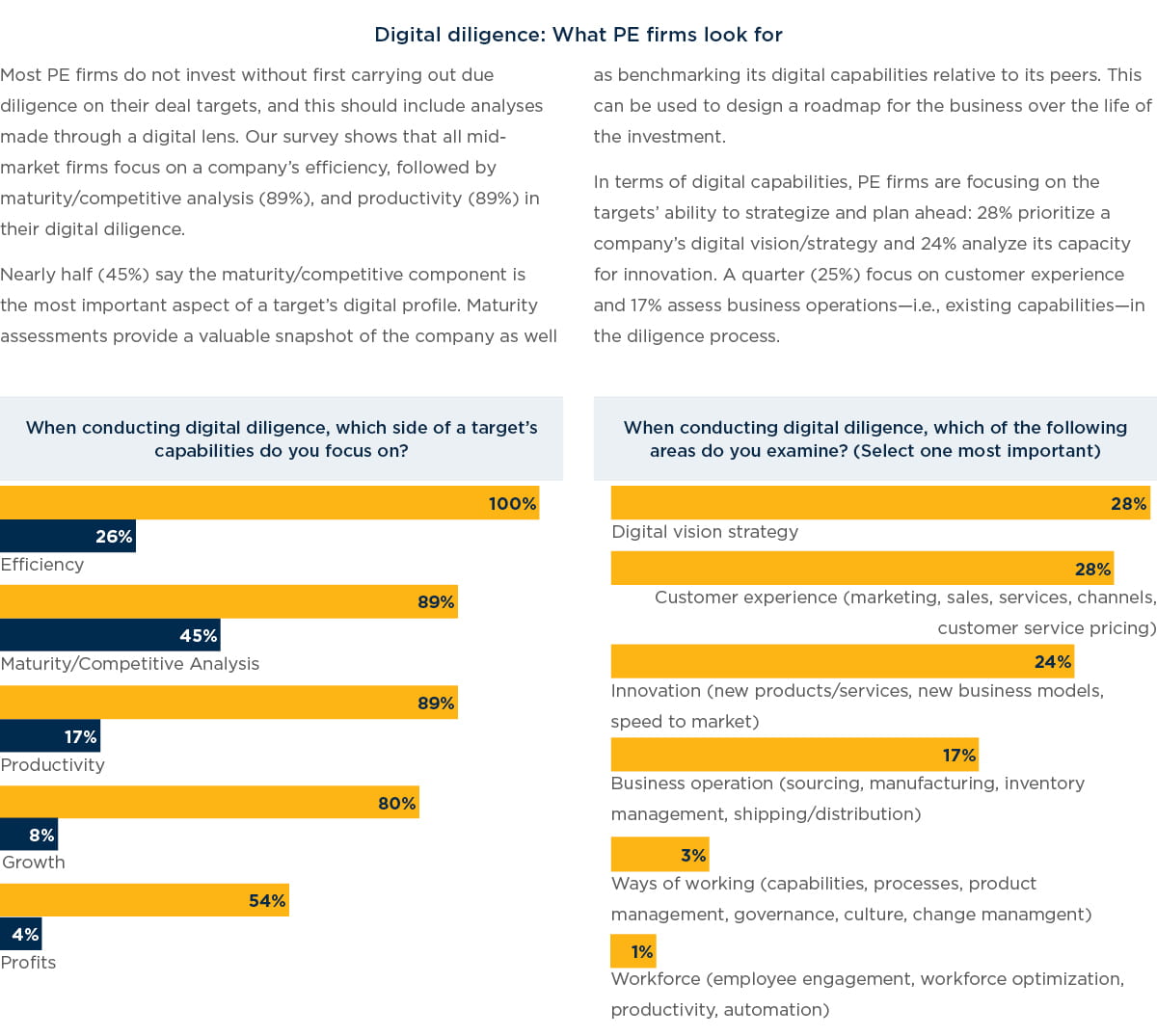

Digital due diligence is a critical first step for PE firms to begin identifying the opportunities with the highest potential for value creation.

At this stage, buyers can conduct a digital maturity assessment and identify how difficult or easy it would be for a business to benefit from digital investment (see "Digital Diligence: What PE Firms Look For”). Post-diligence, PE firms must decide where to invest their digital dollars—and the roadmap will be different for every portfolio company. A software business, for example, may have more agility and ability than a traditional brick-and-mortar company to quickly deliver change or introduce new products to the market.

“While PE investors are innately pragmatic about deciding which projects to execute, they sometimes need assistance from technologists to best understand the business value from digital investments,” says Brad Haller, a director in West Monroe’s mergers and acquisitions practice who primarily works with PE sponsors. “GPs should be prepared to examine all sides of a company, decide where investments make the most sense, and then be rigorous in prioritizing these opportunities based on value potential and feasibility.”

Customer-facing and productivity improvements go hand-in-hand

According to our survey of GPs, customer experience looms large when making digital investments—40% of those surveyed say they prioritize investments that help the portfolio company to keep pace with the expectations of their customers. This may be expected given the rise of highly sophisticated digital companies in recent years.

“Companies such as Amazon and Uber have raised the bar when it comes to satisfying customer needs,” says one PE executive. “Digital methods are well advanced and there are countless examples of highly customer-centric operations. This has made the customer experience completely seamless and has changed expectations.”

Productivity gains are also top-of-mind for PE firms—in our survey, 25% say improving workforce/labor productivity was their top priority, and 18% say they are focused most on reducing operational expenses.

Part of PE’s traditional focus has been on efficiency gains, so it may be tempting for some firms to view digital as a purely cost-saving play. A productivity program is often faster to implement and quicker to produce EBITDA value than a customer-facing program. This is in part because of the inherent lag between launching a product, the adoption of that product by customers, and finally the sales of that new product translating into growth. Conversely, the impact of rationalizing operations within a business are typically felt in near real-time.

Of course, the front and back ends of a company do not exist in isolation and should not be viewed as wholly separate. Ken Goebel, a senior manager in West Monroe’s M&A practice focused on digital capabilities, says that West Monroe’s clients often start from a cost-saving investment premise that then translates into improved customer experience.

“We are often asked how to strip costs out of back-office processes,” he says. “Take a mortgage approval process. By helping a mortgage company re-engineer the process by which customers are approved, they are able to reduce the loan application cycle time. Therefore customers actually end up being much more satisfied on the front end.”

No two companies are the same and each investment will require a tailored approach. No matter where the emphasis is placed at a given portfolio company, a digital program can be value-accretive, producing increased sales, improved margins and higher growth, often in combination. Both front- and back-of-the-house opportunities, and the interplay between the two, should be carefully considered.

The rise of mobile

Regarding the specific technologies that respondents say have brought the most value to their portfolio companies over the last 12-24 months, 23% highlight mobile platforms, followed by cloud-based data and software solutions (20%), advanced analytics (13%), and process automation (13%). This correlates with the aforementioned bias that firms report towards customer-facing investments, since mobile apps are typically aimed at improving customer experience. The rationale for investments into robotic process automation, meanwhile, tends to be optimizing back-end systems to make cost savings —which, as mentioned, may deliver customer benefits.

This emphasis on mobile platform investments should not come as a surprise. In the B2C space, companies are expected to deliver their products and services via apps. Smartphone usage has exploded in the past decade, with 8 in 10 mobile phone connections in the United States now being smartphones. As one PE executive in our survey says: “Cross-platform mobile applications have delivered value in our portfolio companies. Customers are increasingly focused on mobile-based tools and apps and we are using this inclination to develop ones that are user-friendly.”

Chapter 3: How to win at digital: Key stumbling blocks and steps to overcome them

It is clear that digital can unlock future returns at portfolio companies and that digital investment theses, diligence, and strategies are a means of achieving such value creation. Actually putting such strategies into effect can be particularly challenging. There are numerous hurdles to success that must be overcome, but two stand above the rest for PE: speed and culture.

Coping with tight timelines

Perhaps the biggest challenge facing GPs when considering digital investments is how to execute an effective program before the desired time of exit. Fifty percent of PE executives in our survey say that making improvements quickly enough to have an impact before the end of the hold period is the greatest barrier to digital investment.

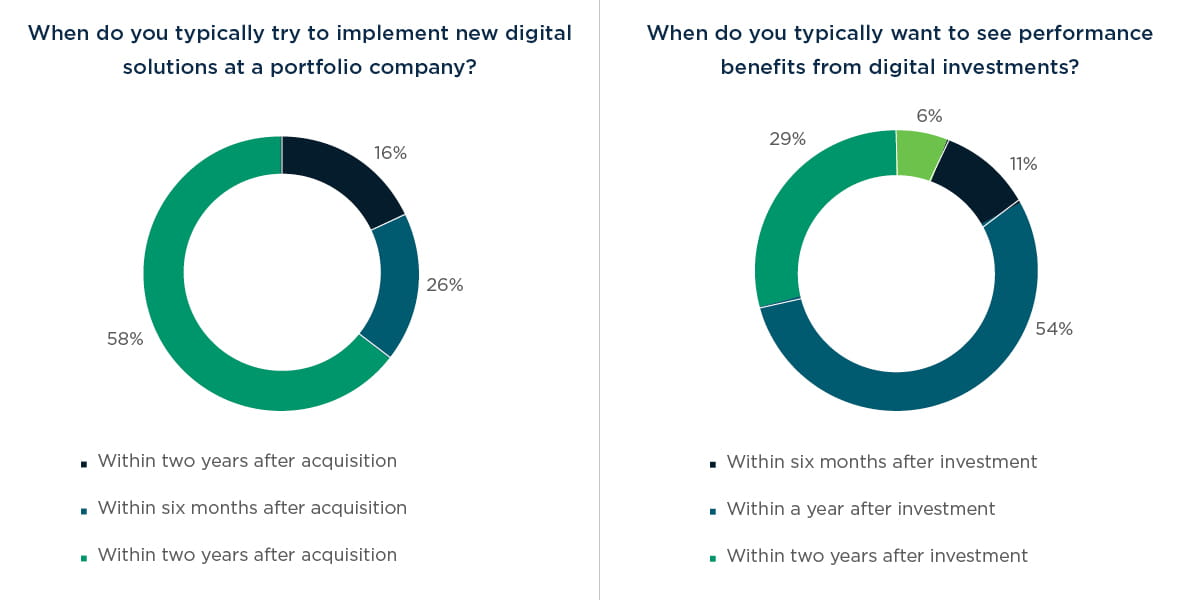

To address this, 84% of respondents say they typically try to implement new digital solutions at a company within the first year after acquisition, and 26% attempt this within as little as six months.

These results underline how time-conscious PE firms are in their pursuit of value creation. Just as 100-day plans are the norm in PE as a means of driving rapid operational change, such plans are essential in implementing and achieving digital performance gains. With respect to the timing of results, nearly two-thirds (65%) of GPs say that they wish to see gains filter through within the first year of investment, and 11% expect to see results within just six months.

This is a tall order, but there are some useful tactics to fulfill it. One approach is for PE firms to develop a digital playbook for each sector or industry segment in which they invest that lays out a game-plan for a digital program in that segment.

“Any given industry typically faces a set of common digital issues, and you can create mental models to address those issues if they are spotted at your investment,” West Monroe’s Haller says. “The solution may not be perfect for every company, but you have at least a running start at solutioning which allows you to be action-oriented.”

Buyers can use the playbook in the targeting and due diligence phase to identify companies for which they have a ready-made digital game plan and put the plan into action immediately after deal close.

In this way, digital strategy is distinct from other aspects of portfolio company management and improvement. Whereas it may make sense to remain hands-off at the start of the hold period in certain areas of a business, when it comes to digital, you need to move quickly and decisively since it may take longer for those ideas to see results than in other parts of the business. Having a deliberate and efficient methodology, and in some cases even a piece of software or a product-based solution, can allow PE owners to launch digital investments in a rapid fashion.

Preparing for exit

PE firms clearly strive to implement digital solutions and achieve results during the hold period—especially given the potential gains to be realized come exit time. More than 8 in 10 respondents to our survey (82%) say they view mature digital investments at a portfolio company as a differentiator or value driver at exit.

Three-quarters (75%), the majority, say they also make digital investments in order to improve the exit price for a portfolio company without the expectation of performance gains before the sale.

This demonstrates the added value that buyers see in digitally mature businesses and the future upside this presents. It is common for PE investors to divest assets with clear value creation potential to make them attractive to new buyers, in particular to fellow financial sponsors. Therefore it stands to reason that digital investments will be pursued even if they fail to fully mature prior to exit— and successfully digitizing a business, or simply making digital investments that will deliver results in the future, can ensure an asset commands a higher sale price.

“When you take a brick-and-mortar business and make it a truly digitally enabled company, that changes the multiple the asset can get at sale,” Haller says. “A traditional retailer is probably going to sell for between 10x and 12x EBITDA, but a software business will transact for around 17x to 18x. A lot of businesses are trying to figure out what they can do to be considered more of a digital business in order to position themselves to achieve that type of multiple.”

Culture – Overcoming resistance from management

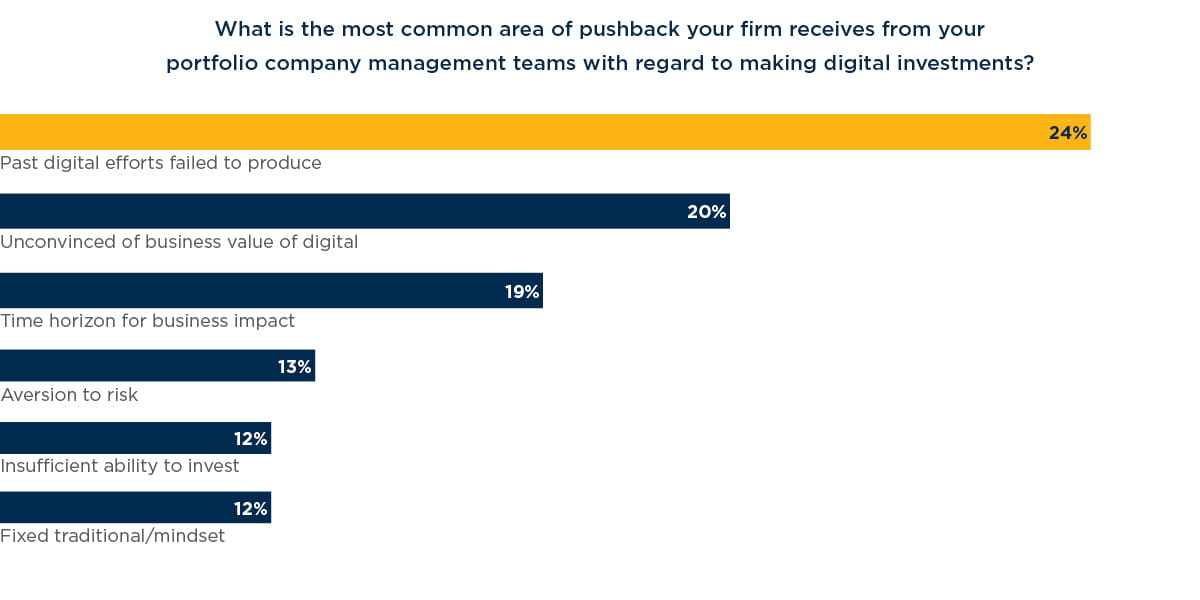

In attempting to drive value through significant digital change at portfolio companies, it is likely that sponsors will, at least some of the time, face resistance from management teams. There are many reasons for this pushback, as discussed earlier, including experience with past digital efforts having failed to produce desired results (24%), being unconvinced of business value from digital (20%) and the time horizon for ROI being too long (19%).

Indeed, in a 2019 Gartner CEO survey, 78% of respondents said that certain digital initiatives they initiated in the last 12 to 18 months had failed to meet business expectations. Digital may be top of mind for leadership and investors, but in reality, it remains hard to define and doesn’t have the best reputation for success.

“There are certain limitations within companies when it comes to the investment culture,” says one PE managing director. “They aren’t always able to identify the right investment options. Even after providing detailed predictions using advanced analytical tools, there is still resistance from management teams who rely on traditional business models.”

Convincing portfolio company management to undertake new efforts at digital investment requires a deliberate process. To start, it can be helpful to provide successful case examples with proven success to the management teams. Another useful step is to examine the company’s digital maturity with its leadership team, to examine possible reasons for previous failures. They may not have appreciated the steps necessary to prepare the company for achieving their digital goals.

Culture—Cultivating a growth mindset

Ultimately, culture is one of the core reasons why digital transformation efforts fail. Most companies have a fixed mindset (“I have seen this before and here is what we should do”) rather than a growth mindset (“I likely don’t know the right way to solve this issue, and I need to be willing to try new approaches and be comfortable with failing”).

“This represents a key opportunity for PE owners— driving home the importance of adopting a growth mindset to achieve digital goals,” Hahn says. “It requires behavioral change to give the organization actual on- the-ground experience with new ways of working and building muscle memory. It will likely be necessary to train executives on how to think and act differently; it may even require replacing members of the management team to successfully achieve this cultural shift, depending on the skill set and openness of the executives involved.”

This new way of working may entail steps such as introducing agile methods of product development, delegating decision making, creating multi-disciplinary teams, and upgrading the skills and capabilities of company staff.

Adopting a new, growth-focused way of thinking is a key tool for coping with the aggressive pace of technological change in today’s world. In our survey of GPs, the two trends respondents say are driving their digital investments are the level of competitive disruption in the marketplace (30%) and the high level of operating inefficiency and excessive costs at their portfolio companies (26%).

Culture – Making effective use of digital resources

Of course, formulating a plan for executing digital investments will be of little value without the capabilities to see that plan through to fruition.

And 33% of the GPs in our survey report that less than half of their portfolio companies possess the internal capabilities sufficient to drive a digital program.

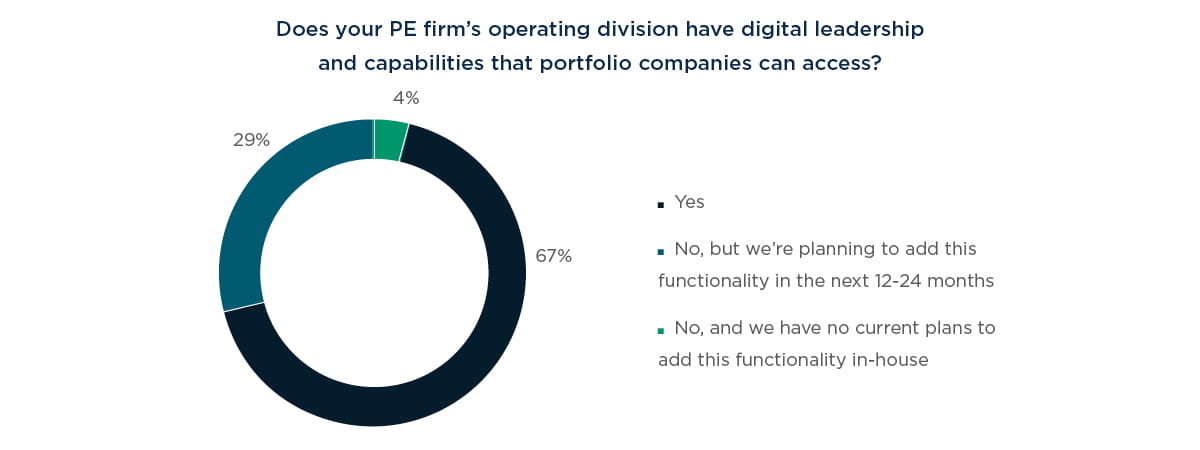

This is where PE owners can add genuine value. As partners to their companies, buyout firms can act both as drivers of change and sounding boards for the validity of strategies developed by management. Encouragingly, our PE respondents are increasingly well-equipped to offer help in this area, with 67% saying their firm’s operating division has digital leadership and capabilities that portfolio companies can access. Another 29% say they are planning to add such functionality within the next 12-24 months.

At the same time, this support does not need to come directly from the PE sponsor. One of the primary assets of a PE firm is its network and its ability to guide investments, with the help of consultants and by hiring in management talent required for achieving results. More than half (53%) of respondents place a high priority on working with outside experts or consultants to plan and implement digital strategy, while 29% prioritize making new digital hires to a company.

One PE executive in our survey highlights the importance of cross-collaboration between portfolio companies, whereby businesses can share best practices and insights into what has delivered results for them: “I feel experience counts in matters of implementation of any kind of strategy, particularly where digital strategies are concerned. We need to make sure that all key parameters are measured. Suitable advice from other portfolio companies helps for purposes of comparison.”

Conclusion

The ability to transform businesses through digital is one of the greatest value creation tools at PE's disposal. The evidence shows that more can be done to formalize, standardize, and prioritize this process, but the broader trend is that PE has recognized the potential of digital.

Now it is focusing on how to realize it. Before making their next digital investment, we recommend that PE firms consider the following best practices:

1. Define "digital" and formalize strategies

Given that a significant portion of PE firms do not have a singular definition of “digital” or documented digital strategies at the portfolio company level, this should be the first priority. Whether you adopt our definition – "Applied technology that changes business conditions, creates an adaptive culture, and uses data to scale and grow, in order to create mutual value" – or opt for your own, it is important that everyone in the firm understands what is meant by the term. Once there is a common definition, it is then crucial that every portfolio company has a documented digital strategy that is tailored to that specific company.

2. Choose wisely

Companies tend to struggle with prioritization: After identifying multiple digital projects, they either default to taking on too many or end up forgoing the right ones. In such instances it is rare that any of this delivers desired results. A better approach is to concentrate on no more than two or three core digital initiatives, whether that be productivity gains in the back end of the business or delivering improved customer experience or enhanced products or services in the customer-facing side of the company. Prioritization is key, and they can lean on proven use cases or business-minded consultants to determine those priorities.

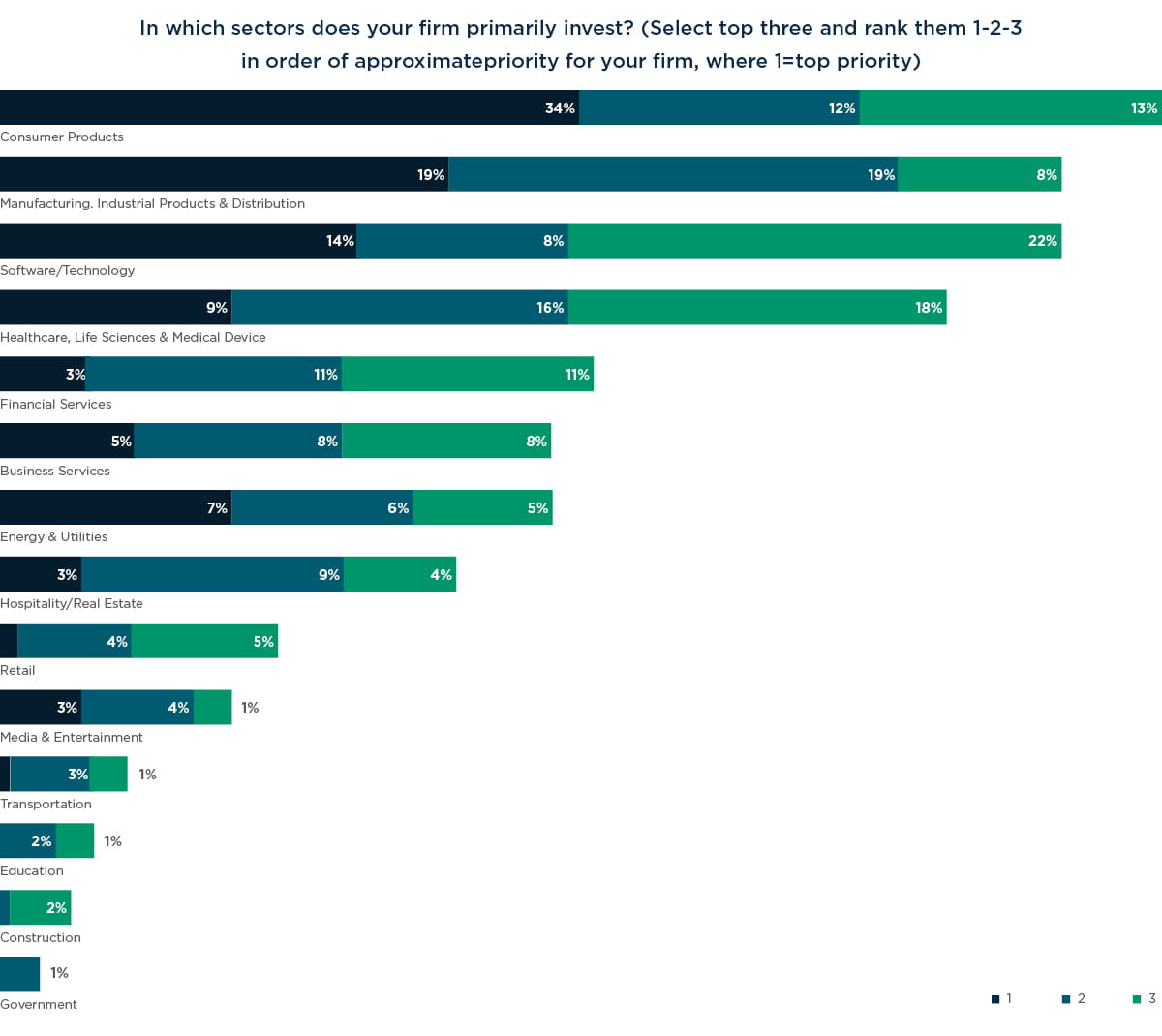

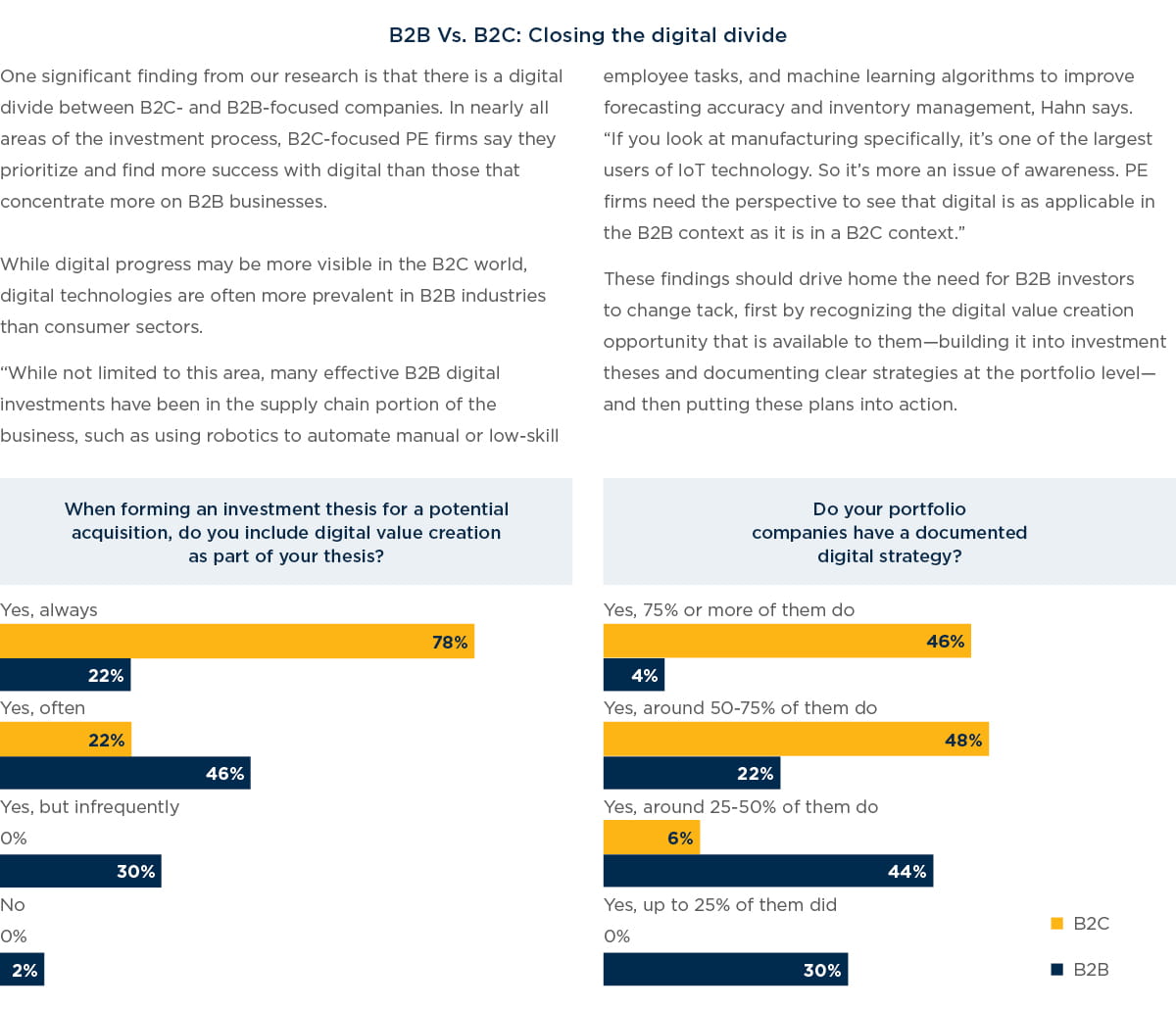

3. Capitalizing on the B2B opportunity

Our survey shows that mid-market PE firms may be underestimating the potential of digital investments in the B2B space. This represents a substantial opportunity. Not only can B2B-focused sponsors incorporate digital more extensively into their investment theses, they can consider how to transform the customer-facing sides of their businesses and not only focus on back-end operations.

4. Speed is everything

Just as it is important to prioritize digital programs to avoid management overload and fatigue, PE firms should also think carefully about how long it will take to implement projects. Digital often requires a substantial change in a business’s operations, organizational structure, skills, capabilities and processes, all of which takes time. Agile, test-and-learn methods are typically the best approach. Bringing in the right resources may be necessary, internally or externally, as digital is a relatively new skill set.

5. Upside at exit

Our survey indicates that PE sponsors are willing to pursue digital investments for their portfolio companies even if such projects do not deliver results prior to exit. Whether or not digital investments have time to fully materialize before the company is put up for sale, growth in digital maturity should be viewed as an asset during the sell-side process. It is important that the company’s digital strategy and progress is clearly articulated to potential buyers, since digital companies typically command higher price multiples.

Methodology

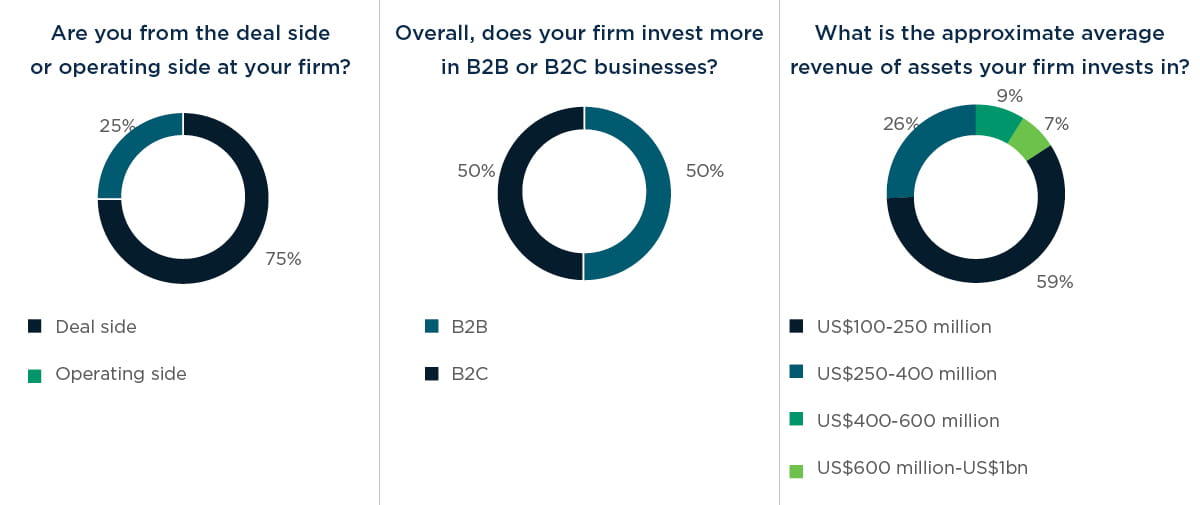

In Q1 2019, Mergermarket surveyed 100 senior PE executives via phone to better understand their approach to digital investments in portfolio companies. Respondents were all based in the United States, and were split between deal-side (75%) and operating-side (25%) personnel. They were also divided between firms that invest more in B2B businesses (50%) and those that invest more in B2C companies (50%).

Appendix