Feb. 26, 2018 | InBrief

Is private equity eating up software, or is software eating up private equity?

Is private equity eating up software, or is software eating up private equity?

The pace of change in technology is faster than ever. Many of us feel this in our daily lives, with a growing expectation that every screen is touch-enabled and an Amazon Alexa or Google Home is always within earshot to take our next command.

This pace of change in technology is supposed to make us more efficient. But the opposite may be happening for tech-focused private equity buyers. Why? Because the resources PE firms have to invest in keeping their portfolio companies’ technology platforms up-to-date keeps growing.

The typical hold period for a PE-owned business is five to seven years. A decade or so ago, the pace of change in technology wasn’t nearly as fast, and PE firms spent less time and fewer resources to keep technology up-to-date during the hold period. Now, the change in technology from Year 1 to Year 5 is drastically different – and the amount of resources and attention devoted to keeping pace with technology for each portfolio company has ballooned.

Think about this way: You buy a modern home and expect to sell in about five years. When year five rolls around, you probably don’t need to do much upgrading to the home to make it attractive to buyers because it was already “modern” when you bought it. But imagine the typical homebuyer’s preferences and expectations changed drastically during that five-year span, as did home décor, and in year five, you had to completely remodel the home to make it attractive enough for buyers. That may be an oversimplified analogy, but it gets the point across.

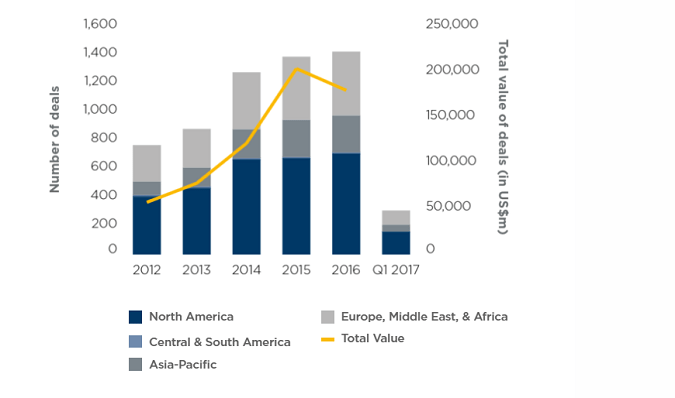

The increased investment due to technology advancements is requiring many PE firms to devote more to due diligence than ever before. Are the company’s systems supporting its product platforms monolithic? Is the technology infrastructure scalable to support double or triple customer growth? How much needs to be invested in product management to grow the company as planned? Despite this increase in complexity, PE buyers are adapting and are not reducing their activity in the sector. Pitchbook recently published data on U.S. deals by sector in 2017, and every sector dipped in volume except one: IT. That is in line with what we see in West Monroe’s M&A practice: Of the 300-plus deals we supported last year, over 20% were directly within the software/IT industry.

Yes, software is the hottest investment sector right now. The demand for software is high, and sellers of software businesses are getting good returns – our PE clients regularly are seeing high double-digit multiples. But the increased complexity that buyers face is also happening in sectors outside of IT. As all sectors increasingly leverage technology to run their operations, software diligence and technology “upkeep” is affecting all sectors. Even if a private equity buyer isn't looking directly at a software/IT investment, they are most certainly spending significant time evaluating the managing the software assets that run the business. For example, a home care franchisor is going to require a complex and scalable set of systems to manage its franchise operations and enable franchises to operate efficiently. Even though the platforms are not the core asset of the business, if they cannot scale, then the business itself will have trouble scaling.

Software-focused investors are commonly asking critical questions in diligence, and buyers investing in other sectors should be asking the same questions:

- What is the ease of integrating technology platforms as I look to integrate add-ons with this platform company?

- Where does the software platform have major technical debt (UX/UI, cloud migration, re-architecture, open-source software risk remediation) that is going to impact my CapEx spend and potentially lower EBITDA margins?

- What re-organization and/or headcount investments are needed (e.g., do I have the right CTO in place)?

To return to the title of this blog post – is private equity eating up software, or is software eating up private equity? – the answer is yes to both. Software and technology costs may be eating up private equity, but it’s not stopping private equity from eating up software businesses that are showing excellent returns.