October 2019 | Point of View

Getting the most from your consultants during a merger

Getting the most from your consultants during a merger

Mergers are stressful by nature—employees are anxious about job security and inevitable culture, technology, leadership, and process changes. Mergers also require seemingly constant attention from all levels, as integrating two or more companies requires making thousands of decisions, then executing them smoothly across the new entity.

Invariably, business-as-usual performance suffers when organizational attention pivots to merger activities. When financial results suffer, leaders frequently tighten the belt on resources until results improve, leading to cycles of increased workload, burnout, attrition, and lower morale.

To avoid this potential downward spiral, organizations engage external resources to help execute a merger, with varying degrees of success. In our experience working with multiple private equity firms that all use consultants differently, we have four best practices that can maximize the ROI from your consultants.

Quantify real business impact using the philosophy "time is money"

Simply put, value is a ratio: a return divided by the corresponding investment. Financially, the ratio is easy to calculate when both the investments and returns are monetary. But what if your investment is dollars, and your return is time? What if your investment is time, and your return is higher employee morale? How do you calculate the value provided? The trick is to convert everything back to a common unit, and the unit of business is dollars.

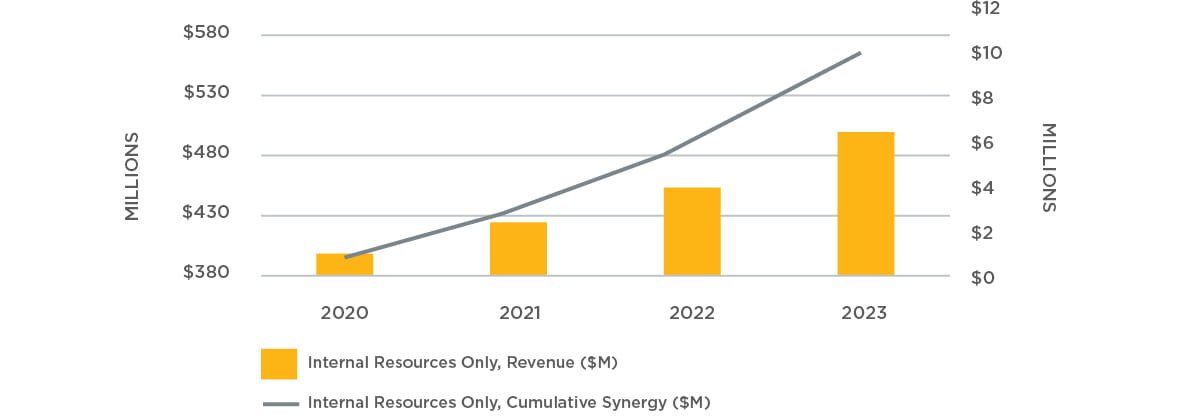

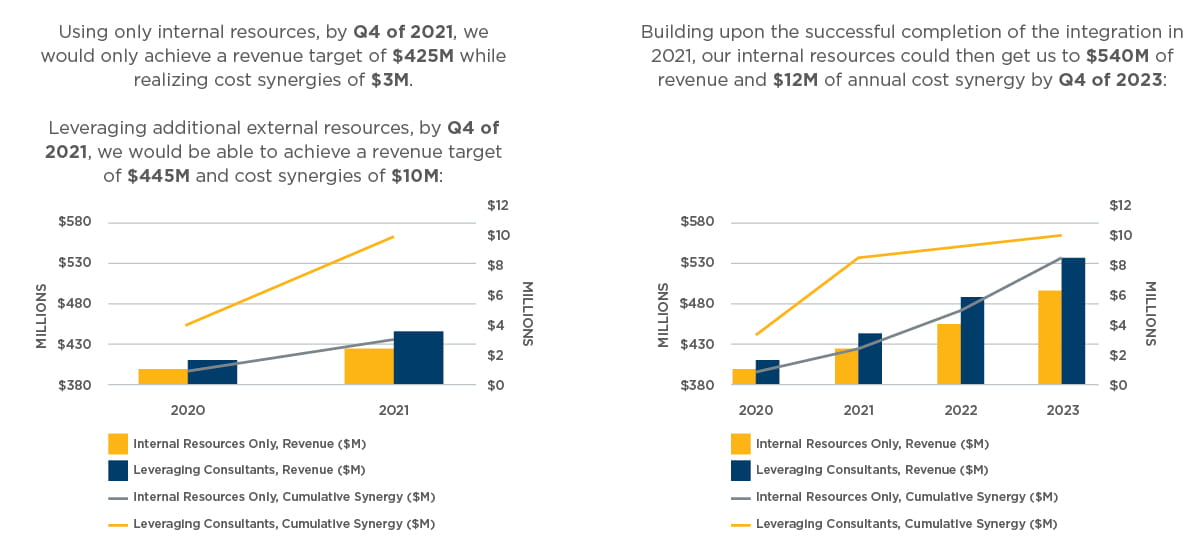

Have you fully considered what it would take to complete your merger relying solely on internal resources?

To start, sketch out what “done” looks like for your integration, along with your critical-path integration projects. Objectively assess the maturity and bandwidth of your resources while also considering run-the-business needs, opportunity costs, and attrition risk. Your baseline statement can be as simple as the following example:

Using only internal resources to achieve a combined revenue target of $500M while realizing cost synergies of $10M, we would need to spend $4M to $6M in one-time integration costs and the merger would be complete in Q4 of 2023.

Each of the baseline variables denoted in bold, should essentially reflect a summation of similar variables across your critical-path projects.

Suppose that by engaging consultants, you could finish your integration projects two years faster than your baseline statement indicated. By considering not only the time value of money but also the additional contributions from internal resources, you can calculate the net present value (NPV) and internal rate of return (IRR) for the investment in professional services:

These aren’t necessarily the only two pro forma statements that can determine the value that can be added by bringing on consultants. With the tight labor market, employee morale and retention are more critical than ever. By considering the financial impacts of attrition, employee engagement can be quantified into a financial unit. (A 5% increase in employee engagement is linked to a 3% increase in revenue growth the following year.)Also, with average private equity hold periods of six years, integration speed is a key component of the investment thesis as synergies and growth patterns need to be established in advance of a profitable exit. A successfully integrated platform with a year or two of stability is less risky to a buyer than handing over a partially integrated work in progress.

Use consultants for the right work

Though every deal has different needs, here are areas where consultants can generally add the most value during an integration:

- Target Operating Model Planning and Playbooks: With experience both across and within your porticos’ industries, consultants can help establish a roadmap for operationalizing the investment thesis, then provide a repeatable playbook for future, smaller acquisitions. Your return is measured in the increased velocity in meeting deal targets and the reduced cost/duration for integration planning in the future.

- Integration Management Office (IMO) Leadership: Consultants leverage a time-tested methodology and toolkit for IMO governance and financial tracking for your merger, and outsourcing the IMO also reduces risk of organizational distraction by ensuring that you have resources who are 100% dedicated to driving integration results. You can measure the value of engaging consultants by leveraging the pro forma statement exercise as outlined above.

- Transfer, Assignment, and Renegotiation of Contracts: If the acquisition was asset-based instead of a stock purchase, supplier contracts and software licenses may need to be assigned to your legal entity or renegotiated entirely, which can be a tedious process. Your combined entity’s scale may also provide increased negotiating power; consultants can ease the burden on your procurement teams and bulldog for discounts or preferable terms. Measure your return in synergies attained via volume discounts or renegotiation of terms.

- Project Delivery: This is the traditional use case for engaging a consulting firm—a temporary need for skilled or specialized labor to plan and execute a project with defined objectives (e.g., product rationalization, ERP implementation, call center modernization). In addition to standard project-related business case calculations, the incremental return from leveraging consultants can be quantified against the long-term cost and project timing impacts of hiring internal resources to perform the work.

- Transformation Adoption: Integrations are a convergence of systems and processes, often requiring sizable investment. In addition to change management toolkits and methodologies, consultants can bring a fresh and independent perspective to ensure all stakeholder concerns are addressed and project business cases are realized. Incremental value creation for OCM and adoption activities is difficult to quantify; costs should be added to the business case calculations for each project.

Assign distinct roles for internal and external resources at the beginning

Before a consulting engagement begins, work with your external partners to identify the level of commitment that will be required from named internal resources. As the buyer of consulting services, you should ensure that the rest of your organization is aware of the work being performed and is prepared to support as needed. Leaders will need to commit time to governance, which includes understanding critical decision factors and quickly making decisions that may have significant impact.

Lower levels of the organization will need to support consultant access to data, processes, and systems; these internal resources can also provide valuable feedback on the details of the engagement scope. If your organization is not highly acquisitive, or if your resources are not used to working with consultants, you may need to invest some additional time in educating your organization on what to expect. Your integration timeline and value capture can quickly get away from you if the right resources are not engaged from the onset.

Hold everyone accountable

Now that you have identified the expected value and gained internal buy-in, it’s time to ensure results.

When establishing a consulting scope of work, be specific and you can expect specific results. Looking back to your pro forma statements, if you expected consultants to accelerate your financial or schedule milestones, then the deliverables from the consultants should reflect that. If the engagement is structured in such a way that you cannot measure the incremental value of the consultants compared to your baseline, the structure of your engagement may need to be revised. Your team of consultants should be autonomous enough that their results can be objectively assessed.

If you hire consultants to find $10M of COGS savings opportunities, and they do, they have fulfilled their engagement. If your internal supply chain team is then only able to enact $2M of those synergies, which team is responsible? If a consulting firm builds a project plan and your internal team struggles to execute it, it’s tough to pinpoint where the breakdown occurred. While it may cost more to expand the consultants’ scope to include execution, resource continuity from planning through execution provides greater clarity around accountability and is a foundation for value creation.

Another means of accountability is the financial structure of the engagement. By leveraging fixed-fee, success-fee, or gain-share billing structures with your consulting partners, they are financially incented to execute their engagement as quickly and successfully as possible.

The final method of accountability is governance. Governance of consultants generally includes weekly status reporting on the engagement progress, monthly reviews or assessments of the consultants’ performance, and a review of internal resource availability. Expect your consultants to do the heavy lifting with your integration, but remember that key decision-making should never be fully outsourced.

It can be challenging to know when to pull the trigger on entrusting external resources with your merger integration. While the expense may seem like an avoidable, additive cost, in our experience the ROI can be quickly proven and you create value, faster. Most organizations underestimate the time, resources, and learning curve it takes for internal resources to handle an integration. Relying on experts who have done this dozens of times before and can help guide your internal resources not only creates financial value but removes headache and stress.